Home>Finance>The Impact of Administrative Law on Personal Finance: Navigating the Legal Maze

Finance

The Impact of Administrative Law on Personal Finance: Navigating the Legal Maze

Published: February 26, 2024

Explore how administrative laws like ERISA, IRS regulations, and the CFPB's role impact personal finance, from retirement planning to investing.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

In the intricate web of our financial lives, administrative law acts as both a guardian and a guide. From the way we save for retirement to the investments we choose and the taxes we pay, the unseen hand of administrative regulations shapes outcomes in profound ways. Understanding these influences isn’t just about compliance; it’s about seizing opportunities and sidestepping pitfalls. Here, we delve into how administrative laws weave through the fabric of personal finance, highlighting the pivotal role of entities like the IRS, ERISA, and the Consumer Financial Protection Bureau (CFPB).

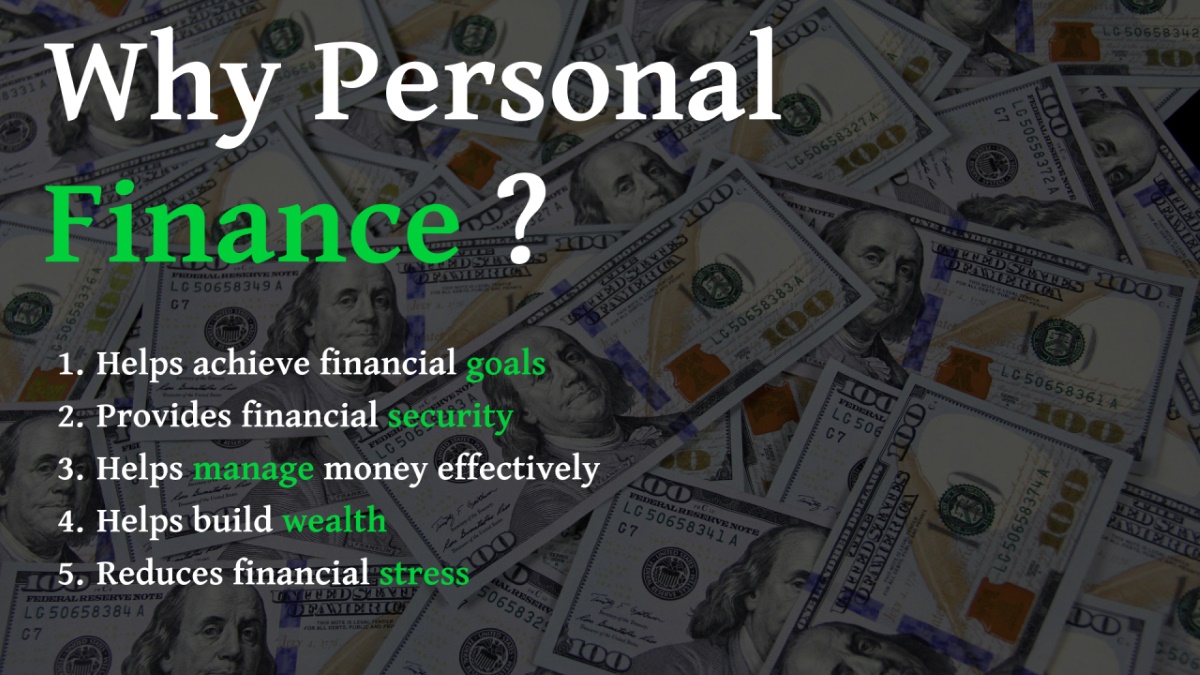

Why Personal Finance is Important

In the grand scheme of things, personal finance is your financial fingerprint—unique, identifying, and crucial to your financial well-being. It encompasses everything from budgeting and saving to investing and planning for retirement. But why is it so important? Simply put, mastering personal finance is key to achieving financial independence, securing a comfortable retirement, and protecting yourself and your loved ones against unforeseen economic downturns.

The Backbone of Retirement Planning: ERISA

The importance of retirement planning cannot be overstated. Enter the Employee Retirement Income Security Act (ERISA) of 1974—a pivotal piece of legislation that safeguards the retirement assets of Americans. ERISA sets minimum standards for most voluntarily established retirement and health plans in private industry to protect individuals in these plans. It ensures that plan fiduciaries do not misuse plan assets and that participants are provided with sufficient information about their plans. Thanks to ERISA, millions of Americans can look forward to retirement with greater confidence.

- Transparency: ERISA mandates that plan participants receive detailed information about plan features and funding.

- Accountability: It holds plan fiduciaries to a high standard of conduct.

- Fairness: ERISA ensures that qualifying employees become vested in their pension plans within a reasonable period.

Investing and the IRS: Taxes as a Consideration

When it comes to investing, the Internal Revenue Service (IRS) plays a crucial role through its regulations. Taxes can significantly affect investment returns, making understanding IRS rules paramount. For instance, the tax benefits of retirement accounts like 401(k)s and IRAs are a direct result of IRS regulations, incentivizing long-term savings. Moreover, the IRS’s treatment of capital gains impacts decisions on when to sell investments, encouraging strategic thinking among investors.

- Tax-Advantaged Accounts: These accounts offer deferred or tax-free growth, affecting investment strategy.

- Capital Gains Tax: The IRS’s rules on short- and long-term capital gains tax encourage holding investments longer.

The Role of the Consumer Financial Protection Bureau (CFPB)

The CFPB, established post-2008 financial crisis, is tasked with ensuring consumers are treated fairly by banks, lenders, and other financial institutions. While what is not a responsibility of the new CFPB includes directly managing personal finance for individuals, its influence is felt across several areas:

- Mortgage Lending: The CFPB’s rules and regulations aim to make the mortgage market more transparent and fair for consumers.

- Credit Cards: It monitors credit card companies, ensuring they don’t employ predatory practices.

- Student Loans: The bureau works to protect students from deceptive lending practices and provides information to help manage student debt.

Navigating the Maze: Strategies for Personal Finance Success

Understanding the impact of administrative law on personal finance is crucial, but leveraging this knowledge for financial success is where the real challenge lies. Here are some strategies:

- Stay Informed: Regularly update yourself on changes in laws and regulations.

- Plan Ahead: Use the protections and opportunities provided by laws like ERISA and tax advantages overseen by the IRS to plan your financial future.

- Seek Professional Advice: Sometimes, the complexity of administrative law warrants professional guidance, particularly for retirement planning and tax strategies.

Conclusion: The Unseen Hand in Your Financial Journey

As we navigate our financial journeys, the unseen hand of administrative law is ever-present, guiding, protecting, and sometimes complicating our path. From ensuring the safety of our retirement savings under ERISA to influencing our investment strategies through IRS tax regulations, and protecting us from financial unfairness under the watchful eye of the CFPB, administrative law is a cornerstone of personal finance. By understanding its role and impact, we can make informed decisions, plan strategically for the future, and ultimately, live well financially.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance